|

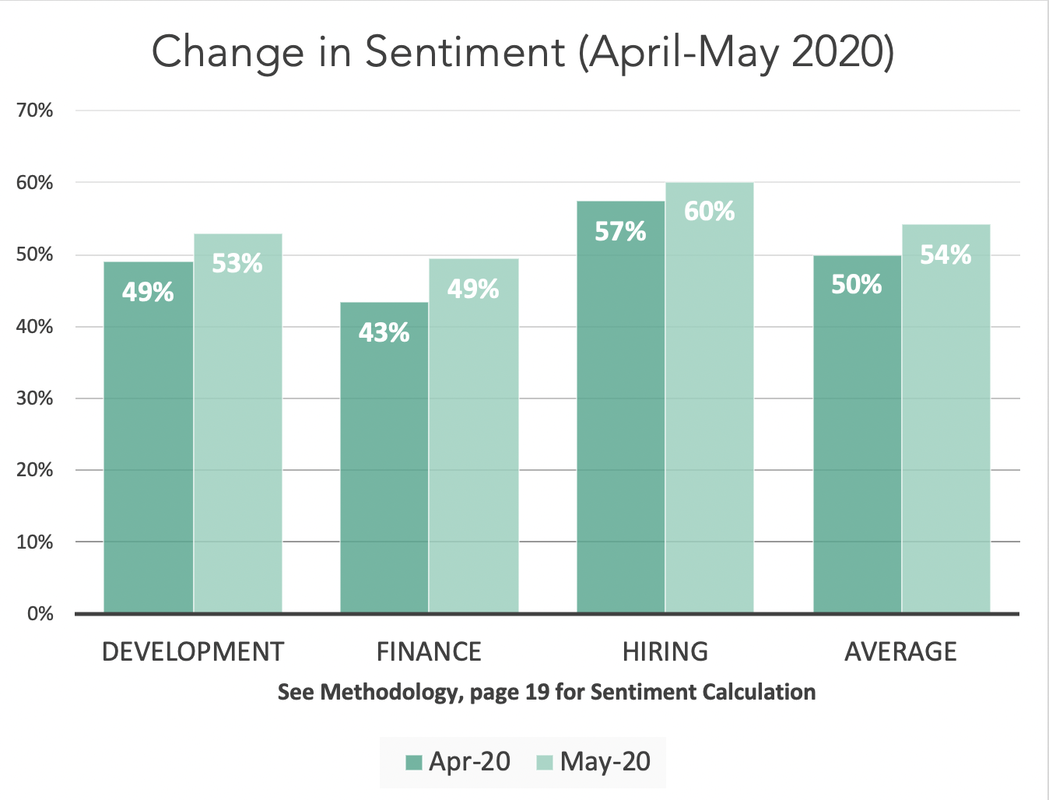

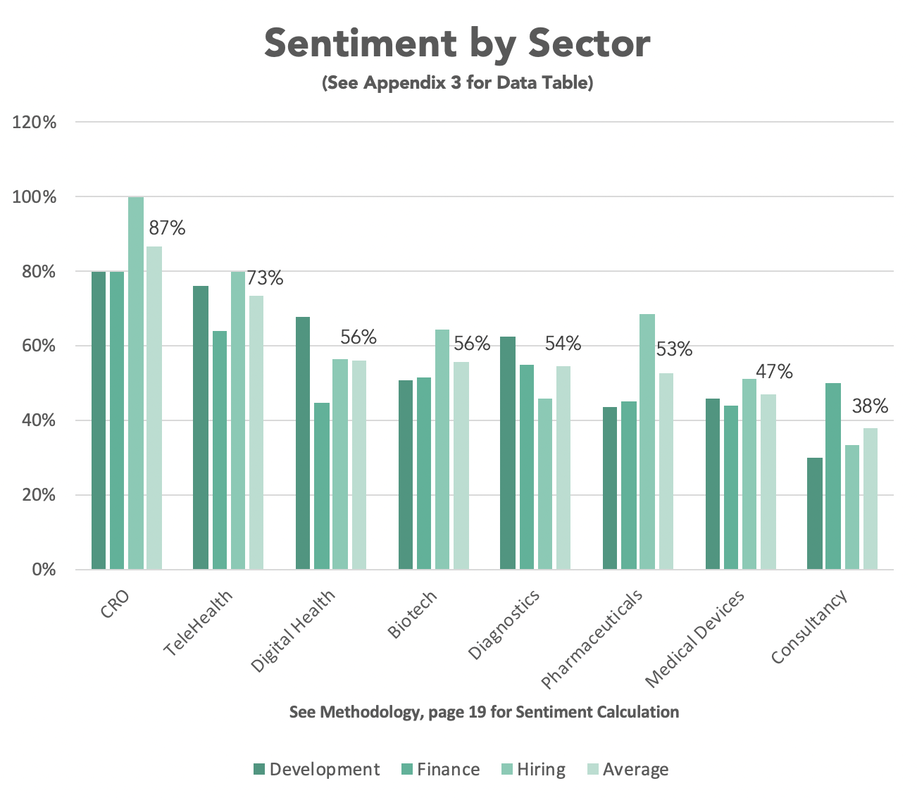

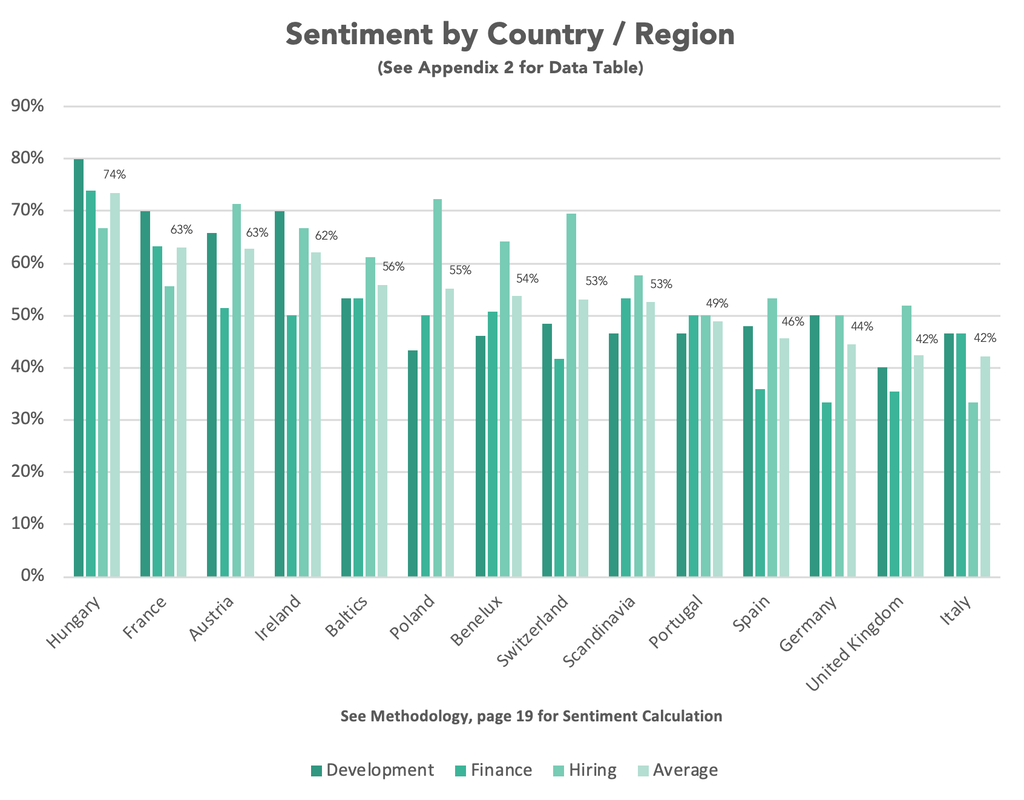

So what difference does a month make? Well, not that much according to our data but the top line story is that there has been a small but consistent improvement in sentiment across all areas of business. When aggregated the overall sentiment index improved from 50% in April to 54% in May. Financing continues to be the major concern but shows the largest jump by six points from 43% to 49%.  SENTIMENT BY SECTOR Our results show a similar pattern to April with the additional data from CROs (87%) and Industry Consultants (38%) top and tailing the industry, reflecting an appetite to outsource research at one extreme, and a reluctance to incur additional costs at the other. Sentiment in Telehealth surged, with an average sentiment of 73% up from 59%, while Digital Health softened slightly from 62% to 56%. Biotech held steady at 56% while Pharma softened from 58% to 53%. Diagnostics improved to 54% from 43% and Medical Devices lifted to 47% from 42%.  SENTIMENT BY REGION Hungary has a strong showing in all areas with an average score of 74%. This may correlate with the low incidence of COVID-19 (total of 486 deaths by 24th May 2020). Amongst big movers, Ireland has lifted from 33% in April to 62% (more diverse sector representation) and Scandinavia drops from 67% to 53%. Switzerland has leapt from 37% to 53%. The Baltics is a newcomer at 56%. The UK and Italy currently rank as lowest sentiment overall at 42% each.  OUTLOOK

The overall mood across the industry in May is distinctly more sanguine than in April 2020. In our discussions with leaders this month there is a recognition that times are going to be tough in the short-term, particularly with regards to securing finance, but that the long-term prospects for the industry are either for a full recovery, or the more prevalent point of view is that life sciences will flourish in a post-COVID world. There is broad agreement that some sectors will ride the white water better than others, and this is certainly borne out by our findings. The challenge for most companies, particularly smaller start-ups, is how to fund themselves through the lean times ahead. Some tough decision making, and creative thinking are required. Founders need to ask themselves if their innovation is still relevant in the new economy. As in any crisis, the strongest, fastest and most adaptable will survive, while the vulnerable (and the unlucky) will be caught out. We don’t sense panic in the marketplace at the moment. On the contrary, many are thinking about or already seizing opportunity. The disruption will create plenty of space for new companies to emerge. There is also a general sense that Europe will emerge as a stronger competitor on the global stage within life sciences and that the industry, as a whole, will receive much more positive attention from investors, the media and the general public.

1 Comment

|

AuthorDr. John Bethell has 28 years experience in health and life sciences recruitment. He is co-founder of two successful recruitment firms employing over 100 staff and delivers training on setting up recruitment systems for start-ups. Archives

October 2022

Categories |

RSS Feed

RSS Feed